Case Study

Reducing Money Wasted on Overdraft Fees

According to the Consumer Financial Protection Bureau, a total of $15 billion was spent in 2016 on fees for bouncing checks and overdrafting. Unfortunately, consumers gain no value from bounced checks.

And while there are some situations in which it may be necessary or prudent for a consumer to overdraft, there are many more situations in which doing so can be very harmful and provide little value.

Most banks charge steep fees for overdrafting, making the overdraft operate like a very small loan with a very high interest rate. What’s more, the overdraft fee is often charged by overdraft incident, rather than proportional to overdraft amount, causing consumers to rack up fees faster than they may realize.

To understand what can be done to reduce unnecessary overdrafting and non- sufficient funds (NSF) fees, we partnered with Freedom First Credit Union, a credit union based in Virginia.

Behavioral Diagnosis and Key Insights

To gain a better understanding of factors that lead to members overdrafting and incurring NSF fees, we conducted site visits to Freedom First branches, interviewed six staff members, and analyzed fee data for all 4,207 Freedom First members who had overdrafted or incurred NSF fees in the previous six months.

The behavioral diagnosis revealed that there were different causes of overdrafting and NSF fees for different groups of members:

1. Some members called in to the Freedom First branches to complain when they were charged these fees. These members were often unaware they were being charged fees for overdrafting or are unaware that their account balance was low.

2. However, over 250 members had more than 50 instances of overdraft or NSF fees in the previous six months. These customers were clearly suffering from deeper financial issues that could not be solved by a heightened awareness of fees or low account balances.

Experiment

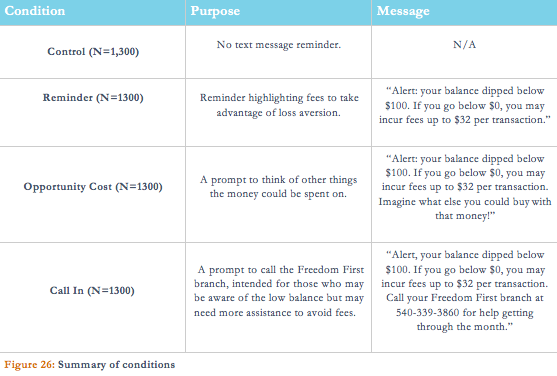

We randomly selected 5,200 credit union members to participate in the first experiment. Those in the treatment groups received text message reminders if their balances dropped below $100.

Reminders were sent no more than once every two weeks, to avoid overloading those who have continually low account balances. To account for the different customer groups identified in the behavioral diagnosis, we implemented three different treatment conditions, along with a control.

Results

This experiment is launched in December 2017 with 5,200 members. We expect to publish our results by Q2 2018.

IN COLLABORATION WITH