Case Study

Requiring Active Choice to Encourage Refinancing

Problem

Customers rarely switch to a new service when it is introduced, even when it is clearly preferable to the service they are already using. One such example is when a financial institution introduces a new low-interest loan. What can motivate individuals to make the switch from a higher-interest loan to a lower-interest loan?

Research

We predicted that a fiduciary (someone who has a legal duty to act in your best interest) would increase the number of switches, as would requiring an active response (which might include some small amount of extra work, whether it’s mailing back a letter, filling out a form, calling a number, or even reading an email). We also predicted that calling attention to the fact that the member is pre-approved on the envelope would be more effective than a blank envelope.

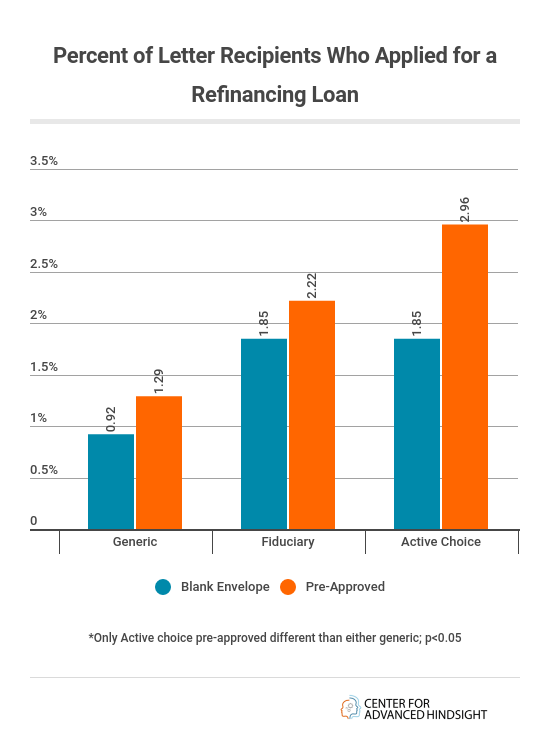

We partnered with Self-Help credit union to design an experiment to increase the number of members who switch to a low interest loan. The experiment had six conditions, a combination of two envelope types (blank or pre-approved) and three letter types.

The letter types were:

1.Control: the reasons to switch.

2.Fiduciary: the trusting relationship between Self-Help and the fiduciary.

3.Fiduciary + Active Choice: both trust and a requirement that the member call in with their decision (to switch or not) regardless of their choice.

Results

While uptake rates were low across all conditions, we did find that the use of active choice with “pre-approved” on the envelope was 3x more effective at getting people to refinance their debt than the control letter with or without “pre-approved” on the envelope. Interestingly, people who received the pre-approved envelope also refinanced larger loans than those without, which suggests that pre-approved messaging may be extra-enticing to households already carrying a lot of debt.

Why it matters

Requiring active choice is a powerful tool that can be used in many situations. While one might not think that making a decision should be a real barrier to change, it turns out that small friction costs can make the difference between action and inaction. If instead we can set up the choice so that the same amount of work is required for selecting the old and new (better) option, we are far more likely to get the desired change.

Anytime we want someone to take an action, we should make sure that the desired outcome is at least as easy as the undesired action, if not more so.

Note: This project was possible through the Common Cents Lab initiative, supported by MetLife Foundation

In Collaboration With